Hello,

My employee earns 1000€.

From these 1000€ I have to deduct:

- 11% for TSU (Social security)

- 11.1% for IRS

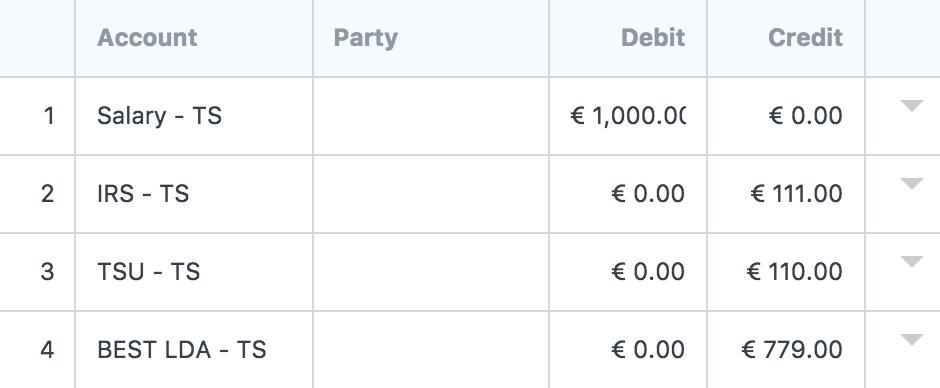

And this is what I get in the Bank payment journal entry:

And that’s ok from the employee’s point-of-view.

But the TSU tax is actually composed of two parts:

- 11% which is paid by the employee

- 23.75% which is paid by the company

While the first 11% are simple to implement as a deduction, I’m confused as to how to implement the second one since, even though it is related to the employee’s base salary… it is not an earning nor a deduction. It is something the company must pay monthly to the state.

How can those 23.75% be implemented in a way that:

- they don’t change the amount paid to the employee.

- they end up being credited to the TSU account

While writing this I had an idea: I could solve it by creating two extra components: TSU_COMPANY1 (earning associated with Salary account) and TSU_COMPANY2 (deduction associating TSU account) and add both to the salary structure with a 23.75% formula. This way the correct amount would move from the Salary account to the TSU account using the proper formula without changing the total paid to the employee. The downside of this solution is that this would show in the salary slip…

Any other solution?

Thanks,

Nuno