Hello Community,

Reiterating over the issue posted here in this post

We are trying to make an enhancement in the Purchase Cycle and would like your feedback on how certain scenarios should be handled and what will be the best accounting practices.

Scenario 1

Creation of Purchase Invoice from a Purchase Receipt where there is change in rates due to currency exchange rate changes

This is what currently happens when a Purchase Invoice is made from a Purchase Receipt with exchange rate difference.

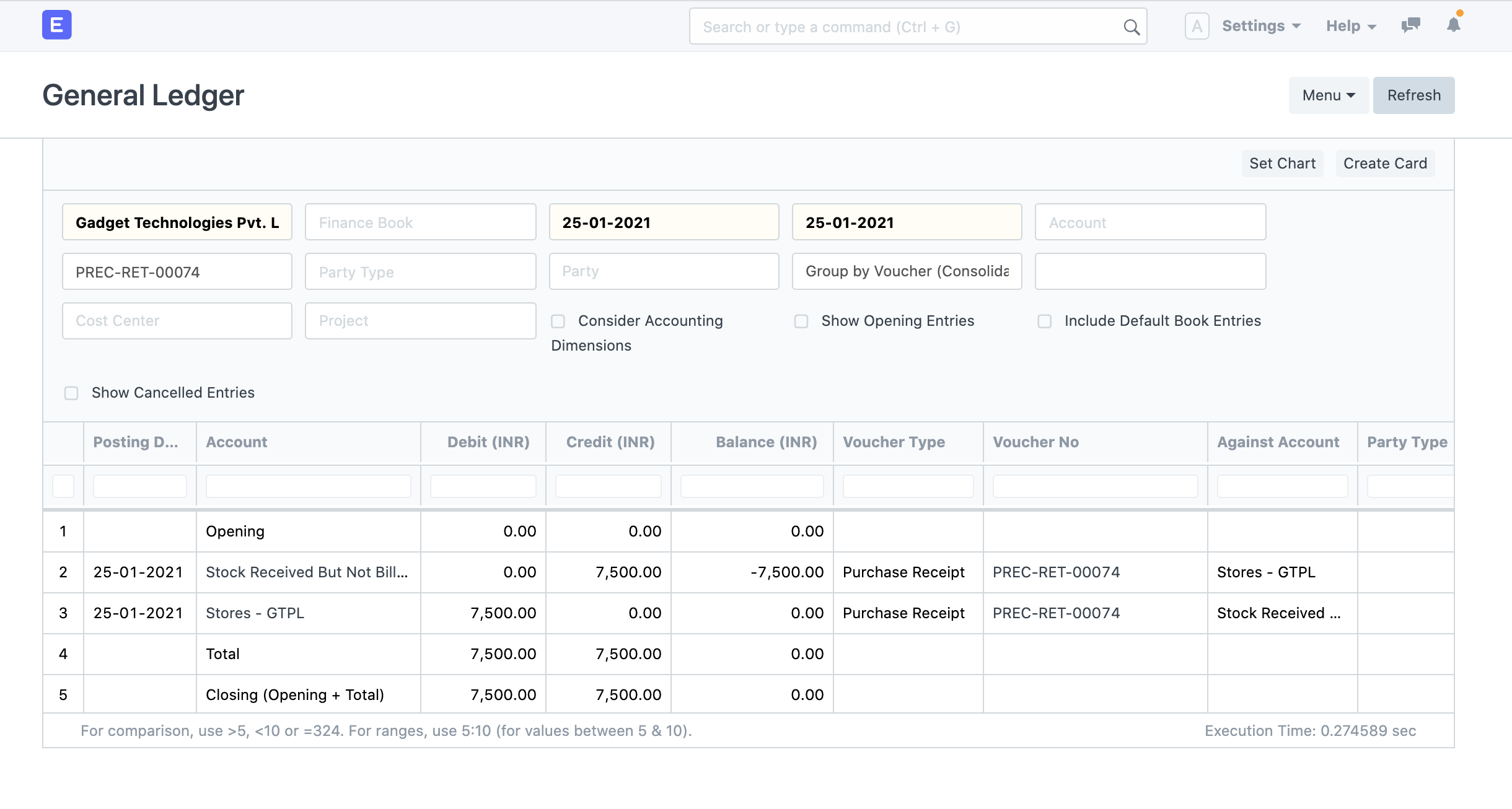

For Eg: Consider an item is being received at $100 at an exchange rate of 75 Rupees per Dollar. The following are the accounting entries posted on submitting the Purchase Receipt

Now suppose at the time of making a Purchase Invoice the exchanges rate changes from 75 Rupees per Dollar to 70 Rupees per Dollar. Then in this case the following Entries are passed

Now even though all the items are fully invoiced there is still an amount of Rupees 500 left in the Stock Received but not billed account. Now the question is what should be done of the remaining 500 Rupees in the Stock Received But Not Billed Account.

Here are the possible options:

Option 1: Debit Stock Received But Not Billed Account for 500 Rupees against Realized Exchange Rate Difference Account (RED) on Posting of Purchase Invoice itself and keep the item valuation based on Purchase Receipt Rate

Option 2: Debit Stock Received But Not Billed Account for 500 Rupees against Stock In Hand Account and repost item valuation on posting Purchase Invoice

Would like the community’s view on which option is followed as the best accounting practice.

Also in case of volatile items the same scenario can happen due to changes in rate of item itself. The rate of items may be different between Purchase Receipt and Purchase Invoice, what should be done in such a scenario from accounting point of view. Should the same process be followed as for the above scenario.

Scenario 2

Creation of Purchase Receipt after a Purchase Invoice with exchange rate difference

Similar Issue will be faced while creating a Purchase Receipt (GRN) after Purchase Invoice. In this scenario what should be the final document deciding the item valuation, rate in Purchase Invoice or the Rate in Purchase Receipt?

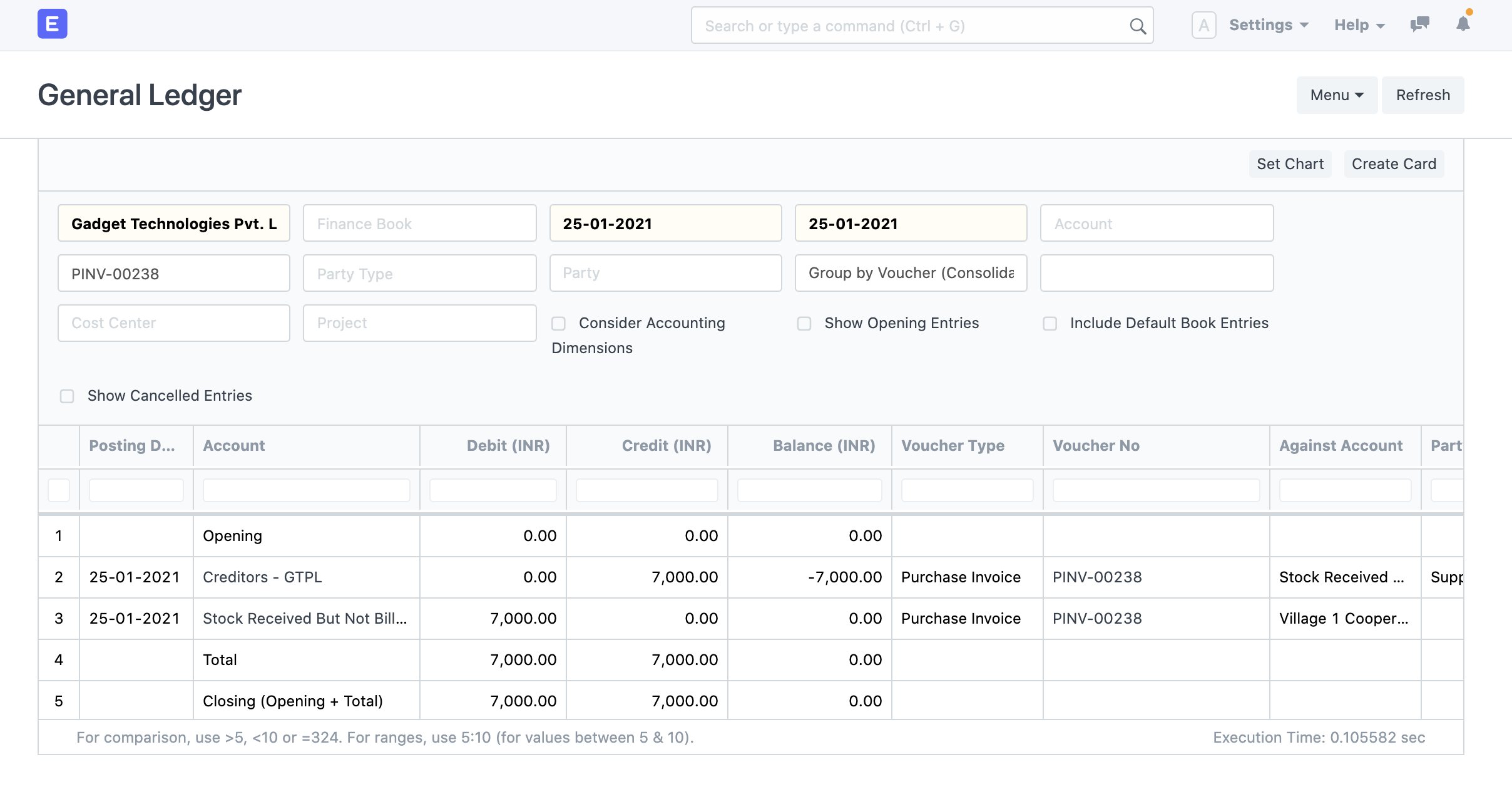

Consider the same example as above these are the possible options available on posting Purchase Receipt:

If Purchase Invoice is considered for final valuation then Stock Received But Not Billed Account will be credited with 7000 Rupees and Stock In Hand Account will be debited with 7000 Rupees

If Purchase Receipt is to be considered for the final valuation then Stock Received But Not Billed Account and RED account will be credited with 7000 and 500 Rupees respectively and Stock In Hand Account be debited with 7500 Rupees